War on Ukraine The Kremlin’s ‘crude’ friendships

Author: Adrià Budry Carbó. Collaboration: Agathe Duparc, March 26, 2022

In the snow, the tracks left by the boots of elite forces and tanks betrayed the large military deployment taking place this winter along the Russian-Ukrainian border. Signs of an impending invasion? Just some military exercises, according to the Kremlin. Putin played for time until the dawn of 24 February.

If snow muffles the sound of boots, the clattering of railroad convoys can rarely be deceptive in the fatal march of history. In January, the state oil company Rosneft quadrupled its rail deliveries of kerosene, diesel, and petrol to the Russian army stationed in seven regions bordering Ukraine and Belarus. In February, these volumes reached 14,000 barrels per day, according to Energy Intelligence, an analytics firm which had warned of the imminent warfare manoeuvre.

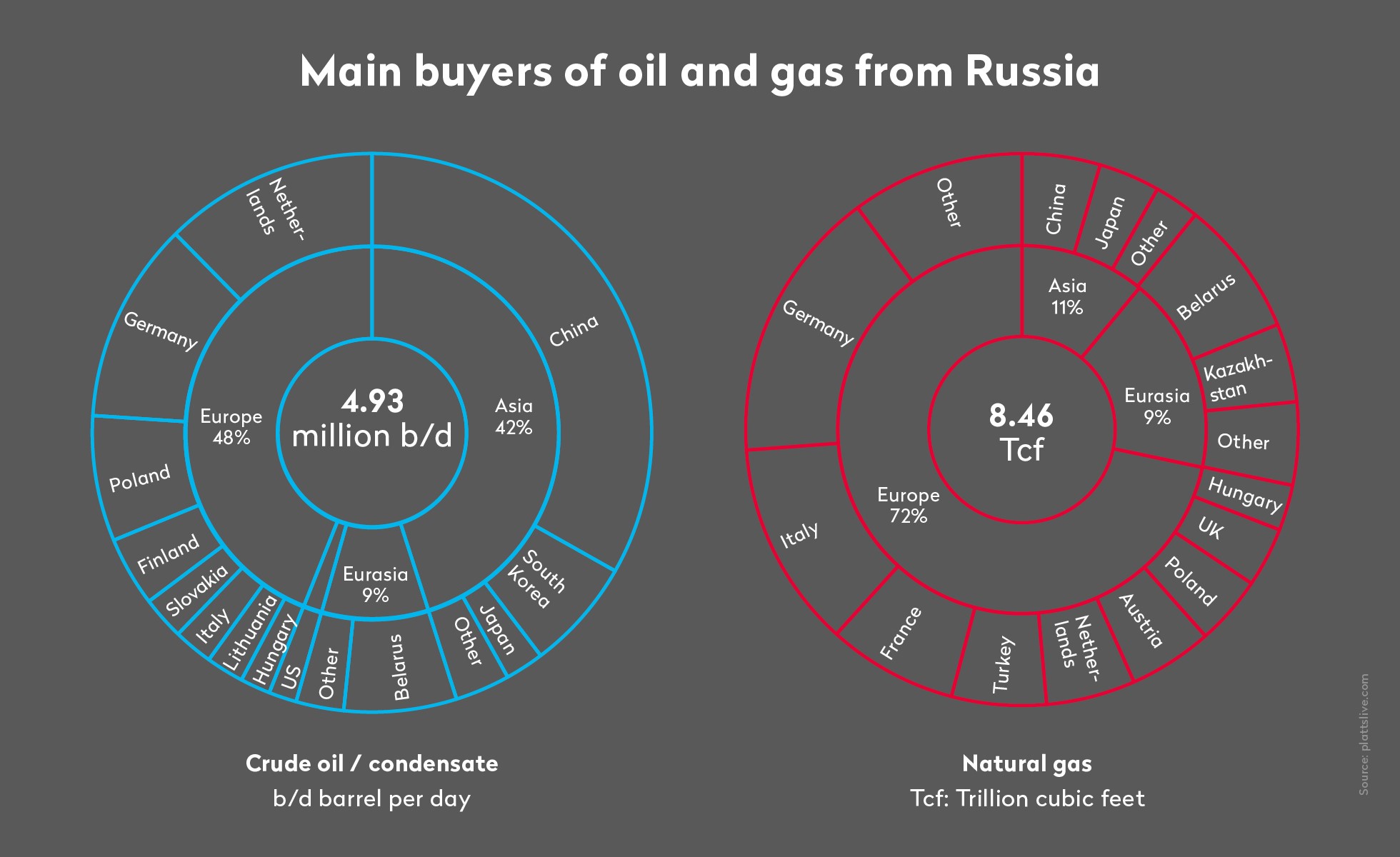

In traders' circles, commodities are usually referred to as the blood of the economy. In Russia, a country which produces some 10% of the world's hydrocarbons, oil and gas flows are also the fuel of war. They generate US $200 billion a year. In 2021, 36% of the country's budget depended on these exports, and even more so today, as a result of soaring prices and of the ruined Russian economy.

Follow the barrel

Founded in 1993 and built on the ruins of private oil company Youkos, itself confiscated from an oligarch, Rosneft is the backbone of Vladimir Putin's state capitalism. Since 2014, the year in which Russia annexed Crimea, the oil giant has been officially supplying the Ministry of Defence. With prices rising last year, its revenues jumped by 46% to reach staggering US $121 billion, which is twice the country's military budget. When BP acquired a stake in 2011, The Economist warned the British oil giant: "Rosneft is not an ordinary company."

However, it has always been able to rely on the major Swiss-based trading houses to sell most of its oil or to receive advance funds. From 2011, Rosneft also chose Geneva to establish its subsidiaries selling its crude oil.

According to the Swiss Embassy in Moscow, around 80% of Russian commodities are sold via Geneva, Zug, and Lugano. A figure which has been circulating for several years now, without any detailed database available or a breakdown between the different fossil fuels (oil, gas, coal). With regard to crude oil and petroleum products, Public Eye's estimates are currently around 50 to 60%.

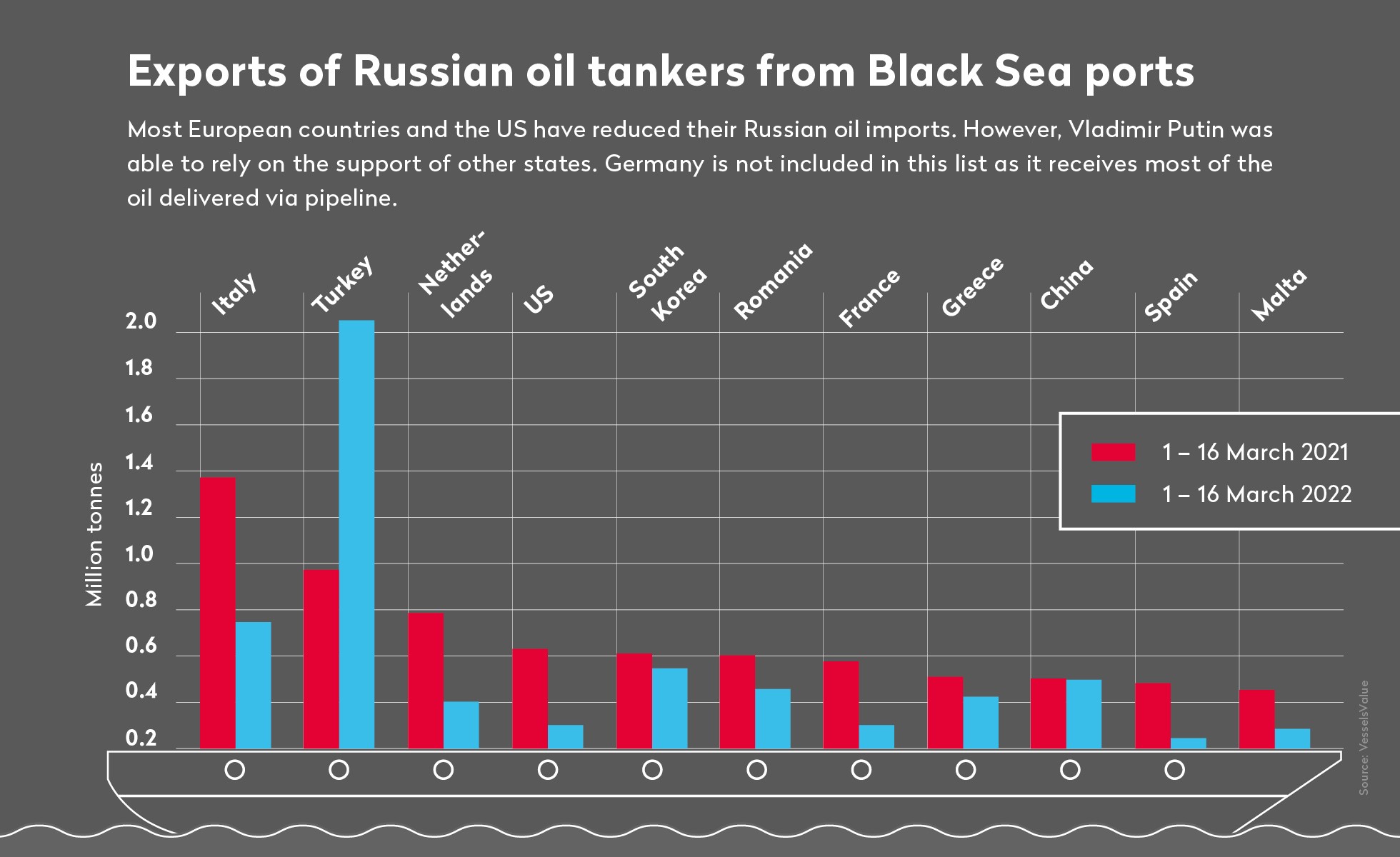

Our investigation shows that oil flows are far from having dried up since the beginning of the war. According to our calculations, which are based on Greenpeace's automated tanker tracker, 326 vessels left Russian ports between 24 February and 21 March, 26 of which were loaded with liquefied natural gas. In accordance with the US import embargo, most European countries have at least halved their purchases of Russian crude oil compared to 2021 (see graph below). But the Kremlin was able to limit the resulting losses by rapidly reorganising the Russian oil flows. Turkey, for example, increased its imports of loaded oil in its Black Sea ports by 240% compared to March 2021, based on data provided to Public Eye by VesselsValue, a website specialized in sea and air cargos. Swiss-based traders have played a key role by helping with the logistics in these troubled times.

The ballet of the Swiss oil traders in the Black Sea

Based on data from shipping brokers for the months of February and March, which the British investigative media SourceMaterial shared with us, Swiss-based traders are among the largest buyers of Russian oil. Leading the way is Geneva-based company Litasco, the trading arm of Lukoil. According to estimates, Russia's largest private producer traded no less than 3.36 million tonnes of Russian oil in February and March. That is about 24.6 million barrels or the equivalent of about 41 Aframax tankers.

They are followed by the independent traders Vitol and Trafigura (around 17.2 and 12.8 million barrels, respectively). Rosneft is also included in the ranking, although the state-owned corporation seems to have been having a hard time finding terminals to unload its goods. More surprisingly, a little-known company called Paramount, also domiciled in Geneva, acquired 11.7 million barrels in February and March. Since the 24 February invasion, Trafigura’s, Paramount’s and Litasco’s volumes have actually appeared to be even increasing.

In the ports of Taman and Tuapse, the Swiss oil ballet seems barely disrupted by the war taking place on the other side of the Black Sea. Tankers chartered by Vitol, Trafigura, and Glencore keep loading Russian diesel and naphtha shipments, according to data from SourceMaterial. Towards the end of 2021, these three companies won tenders for these lighter petroleum products from Rosneft, which runs a refinery on the eastern side of the Black Sea.

©

Yegor Aleyev / Keystone

©

Yegor Aleyev / Keystone

Contacted by Public Eye, Trafigura claims, through its spokesperson, to dispute the figures in our possession but did not provide us with details of those volumes shipped, which "month after month remain in accordance with our contractual agreement". Paramount, in contrast, confirms the figures but is contesting the trend. "There has been no specific increase since the start of the war in Ukraine", maintains its representative. While Litasco did not respond to our requests for comment, Glencore did not respond to a detailed list of questions but provided us with a statement claiming that the group "will not enter into any new trading business in respect of Russian origin commodities unless directed by the relevant government authorities".

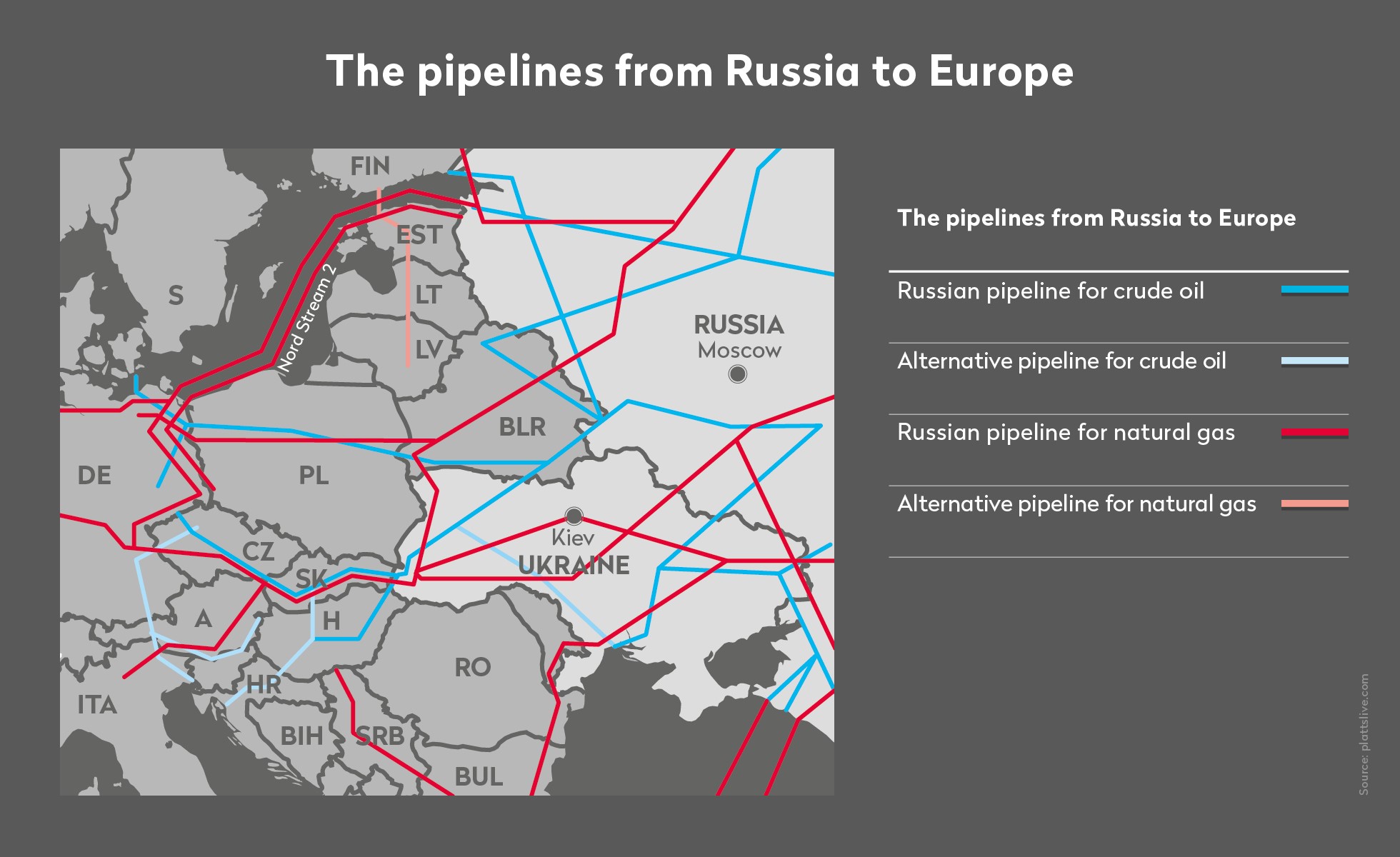

On the Black Sea, the tankers are bound for Turkey, Lebanon, and southern Europe. Malta, Greece, and Italy are the countries that most depend on the approximately 7.8 million barrels of crude oil and petroleum products exported by Russia before the crisis. "From a European perspective, you could think of a decline in Russian oil", admits Vitol's CEO Russell Hardy, "however, it is difficult to change the flows of pipelines and many refineries have no alternatives". On 22 March, at the annual FT Commodities Global Summit in Lausanne, he reiterated that Europe was dependent on Russian diesel to a degree corresponding to half of its consumption.

The double-talk of traders

According to estimates by Source Material, Vitol has loaded, since the beginning of the war, no less than seven oil tankers from Russia, with a total value of around US $100 million. Contacted, the spokesperson for the group confirms the current loading of oil in Russian ports but maintains that a "large part is of Kazakh origin, within the framework of existing forward contracts". "As far as possible, we are looking for non-Russian sources of supply", says Vitol, which, like its competitors, says it is working to meet European and global energy needs.

With the notable exception of Vitol, the Swiss-based traders Glencore, Trafigura, and Gunvor denounced in statements the violence of the war in Ukraine and its 'devastating human consequences'. While having announced a review of their holdings in certain companies or their investments in Russia, traders have remained silent about the supply contracts binding to the Kremlin, so-called 'spot' contracts, where both parties agree on a short-term delivery sale.

At present and despite the US embargo on Russian crude oil imports, this trade is not illegal to other countries. However, a certain effervescence is currently palpable on the trading desks and in the compliance departments of large commodity houses. Risk managers say they have been doing “weeks of over fifty hours since the invasion", because "it's in uncertain times like this that traders can make the most money". Most companies, however, deny negotiating new contracts on Russian crude oil or products.

The FT Global Commodities Summit saw the directors of various institutions all take to the stage proclaiming they will sign no new spot contracts with the Kremlin’s state-owned companies, stating that they were forced to honour longer-term agreements signed before the war.

Not ordinary companies

Swiss traders have always had an intimate relationship with the Kremlin. However, none has probably reached such a level of dependence on Russian oil as Gunvor did fifteen years ago. Co-founded in 2000 by Vladimir Putin's close oligarch friend Gennadi Timchenko, the trading house based in Geneva was quickly allocated up to one third of Russian oil, increasing its turnover tenfold, which in 2007, at the height of this special relationship, had already reached US $43 billion.

While attempting to secure Congolese oil from Brazzaville, Gunvor presented itself in 2010 as a "structure controlled in the background by Putin", declaring to Congolese officials that by allying themselves with them they would see "the doors of Russia open for economic cooperation agreements".

Identified as a company close to the Kremlin, Gunvor decided to undertake a rapid diversification throughout the African continent and in Latin America. Then, in 2011, Rosneft established its trading department in Geneva, opening its tenders to more companies. In 2014, after the invasion of Crimea, Gennadi Timchenko was placed on the US sanctions list. Gunvor and its troublesome oligarch were forced to part. He sold his 44% stake to his Swedish associate Torbjörn Törnqvist for the modest sum of one billion dollars, officially just a few hours before the sanctions were enforced.

At Gunvor, 2021 marked the resurgence of Russian hydrocarbons with a 163% increase, following several tenders won in late 2020 and early 2021. According to documents of the trader seen by Public Eye, the Russian share of Gunvor's total supply added up to 13.2%. However, at the rostrum of the FT Commodities Global Summit, its director minimised this exposure. It seems clear that Gunvor is no longer the Kremlin's favourite trader.

A place in the heart of the Kremlin

As it is in the nature of the trading business to fill the gaps, its competitor Trafigura quickly took up the Swiss place in the heart of the Kremlin, using a financial instrument popularised by Marc Rich, the founder of Glencore: prepayments.

While Rosneft was struggling due to a high debt ratio resulting from its expansion, the trader from Geneva offered the Russians in 2013 a unique deal: a financial advance of 1.5 billion dollars repayable in future deliveries of barrels. With this lifeline for the producer, Trafigura secured a stable oil supply at a fixed price.

But business did not end there. At the end of 2016, Glencore acquired a stake in Rosneft, which was struggling to get finance due to sanctions following the invasion of Crimea. Joining forces with Qatar's sovereign wealth fund, the Zug-based giant acquired 19.5% of the shares of the state-owned company (behind the 50% of the Kremlin and the 19.75% of BP) and secured access to some 220,000 barrels of oil per day.

©

AlexanderNemenov / AFP GettyImages

©

AlexanderNemenov / AFP GettyImages

Mainly, it’s the ‘acrobatic’ aspect of the transaction which is questionable. Glencore placed only 300 million euros (avoiding the US dollar subject to sanctions) in shares on the table, Qatar 2.5 billion dollars and the rest was provided by the Russian state-owned bank VTB. Today subject to sanctions, it lent 11 billion dollars to this operation, which is the largest bank loan ever obtained by a Swiss trading company. Putin was so happy with that deal that he personally awarded a medal to Ivan Glasenberg, then CEO of Glencore. In September 2018, the 14% of the shares of Glencore (which still retained 0.57%) were assigned to a subsidiary of the Qatari sovereign fund, sealing a new stage in this intriguing deal.

The last frontier of fossil fuels

When Vladimir Putin launched, by decree dated October 2020, the conquest of hydrocarbons trapped in the Arctic continental ice, it is, of course, again Trafigura and then Vitol (via a consortium) which got on board. That, according to Reuters, the simultaneous negotiations with Gunvor and Glencore were not successful, was not a problem: Trafigura invested 7 billion dollars for 10% of the shares, the largest investment in its history; as for Vitol, with half of that amount.

Indeed, the Vostok Oil project is very attractive to fossil energy traders. Putin dreams big: up to 150 billion dollars of investment, the construction of 15 industrial cities and 800 km of pipelines, in order to extract, eventually, two million barrels a day to finally outpace competitors from the Middle East and the United States on the black gold market. All thanks to global warming and the consequent retreat of the ice.

Just few banks wanted to support such an operation. Trafigura only stated that it had been "mostly financed by long-term debt", without naming any of the creditors. According to Bloomberg, it was again a Russian bank, Credit Bank of Moscow, which advanced the money to the trader.

Banks exposed

However, banks keep making profits with Russian fossil fuels. According to data from Dutch research firm Profundo, Credit Suisse and UBS jointly lent more than 29 billion dollars to Russian oil and gas companies between 2016 and 2021. BNP Paribas, which closed its commodity finance department in Geneva at the end of 2020, is the third most exposed financial institution regarding Russian hydrocarbons, with nearly 47 billion dollars in loans over the same period. With 508 million dollars, private bank Pictet is even third in the European ranking of shares held (for) in Russian groups active in fossil fuels.

But since the 24 February invasion of Ukraine and Switzerland’s application of the EU sanctions, banks have become more cautious. Even if they were not legally forbidden to buy Russian crude oil or petroleum products, they suddenly squeezed the credit flow. "Banks have made it clear that they no longer intend to finance Russian crude oil or any flow from Russia", Gunvor CFO Muriel Schwab stated on 23 March.

As a result, it has become much more difficult for traders to finance transactions, to secure shipments, and to find a ship or even a terminal to deliver Russian crude oil.

The prices of Gunvor’s, Glencore’s, and Trafigura's bonds, all traded by Credit Suisse, collapsed, as revealed by the finance website Inside Paradeplatz. Moreover, trading companies are increasingly facing margin calls. In times of huge volatility with the price of a barrel of Brent crude fluctuating by several dozen percentage points, the costs for a shipment of oil can easily double. The same applies to the cash requirements imposed by banks in order to secure operations.

Margin calls, fire alarm

According to Bloomberg, Trafigura suffered from billions of dollars in margin calls due to soaring prices, and therefore needed to obtain liquidity to hedge its cargo positions. On 8 March, the trader announced 1.2 billion dollars in loans (eventually increased to 2.3 billion dollars on 23 March) from a consortium of banks, in order to deal with the "extreme volatility in the global economy due to the Ukraine crisis". Reportedly, Trafigura is currently also talking with private investors interested in entering capital to the amount of 2 or 3 billion, again according to Bloomberg. This would be a first.

While international pressure was gradually mounting on Russian oil, Trafigura, in early March, managed to get rid of a Russian crude cargo shipment offering a discount of more than 28 dollars per barrel compared to the Brent benchmark. The buyer was Shell, although the Dutch oil mayor was one of the first to announce their withdrawal from Russian business. After huge public criticism Shell eventually vowed, after apologising, that they would not be buying again. BP also declared a stop of purchases of Russian oil on the spot market. According to Bloomberg journalist Helen Robertson, the barrel of Urals on 22 March sold at a discount of US $31. Litasco was still seeking buyers.

Most Swiss traders, however, seem to want to comply with their contracts all the way. Unless sanctions on Russian oil prevent them from doing so. In the corridors of the FT Commodities Global Summit, this is a fate everyone seems to be preparing for. Consultant Jean-François Lambert summed up the feeling: "We cannot continue to deliver Stinger missile launchers from the left hand and buy hydrocarbons from the right hand". In the snow of Ukraine, the outcome of this dilemma becomes bloodier by the day.