Are banks ‘too big to jail’?

July 29, 2021

©

Keystone / Urs Bucher

©

Keystone / Urs Bucher

In Switzerland, regulation in the field of the fight against money laundering is based on two pillars:

- According to federal law on the fight against money laundering and the financing of terrorism in the financial sector (the Anti-Money Laundering Act, AMLA) so-called financial intermediaries such as banks must comply with due diligence and reporting requirements. FINMA, Switzerland’s financial supervisory authority, is responsible for overall supervision of compliance with specific obligations in these areas. FINMA also supervises compliance of large and medium-sized banks with AMLA; apart from this it relies on self-regulatory organisations and supervises their activities.

- In addition, money laundering is a criminal offence and as a result is prosecuted and sanctioned by the law enforcement authorities.

Supervision by FINMA

If, in the course of its supervision and oversight, FINMA encounters violations of legislation and irregularities, it has recourse to measures to eliminate these and to sanction the guilty financial intermediary. After an initial informal declaration of the suspicion, FINMA can initiate and implement ‘enforcement proceedings’. Various possible sanctions are available under this process. They include: industry bans, cease and desist orders and activity bans, publication of rulings, the disgorgement of profits, and withdrawal of authorisation, liquidation and bankruptcy.

Swiss banks face difficulties due to large corruption scandals

Yet again, large-scale corruption scandals of recent years have left Switzerland’s financial centre in a negative light. In recent years, FINMA has announced enforcement proceedings against a range of banks and bank managers. These have been triggered by (alleged) cases of corruption around the international football association FIFA, the Brazilian oil company Petrobras, the Venezuelan oil company PDVSA and the Malaysian state fund 1MDB.

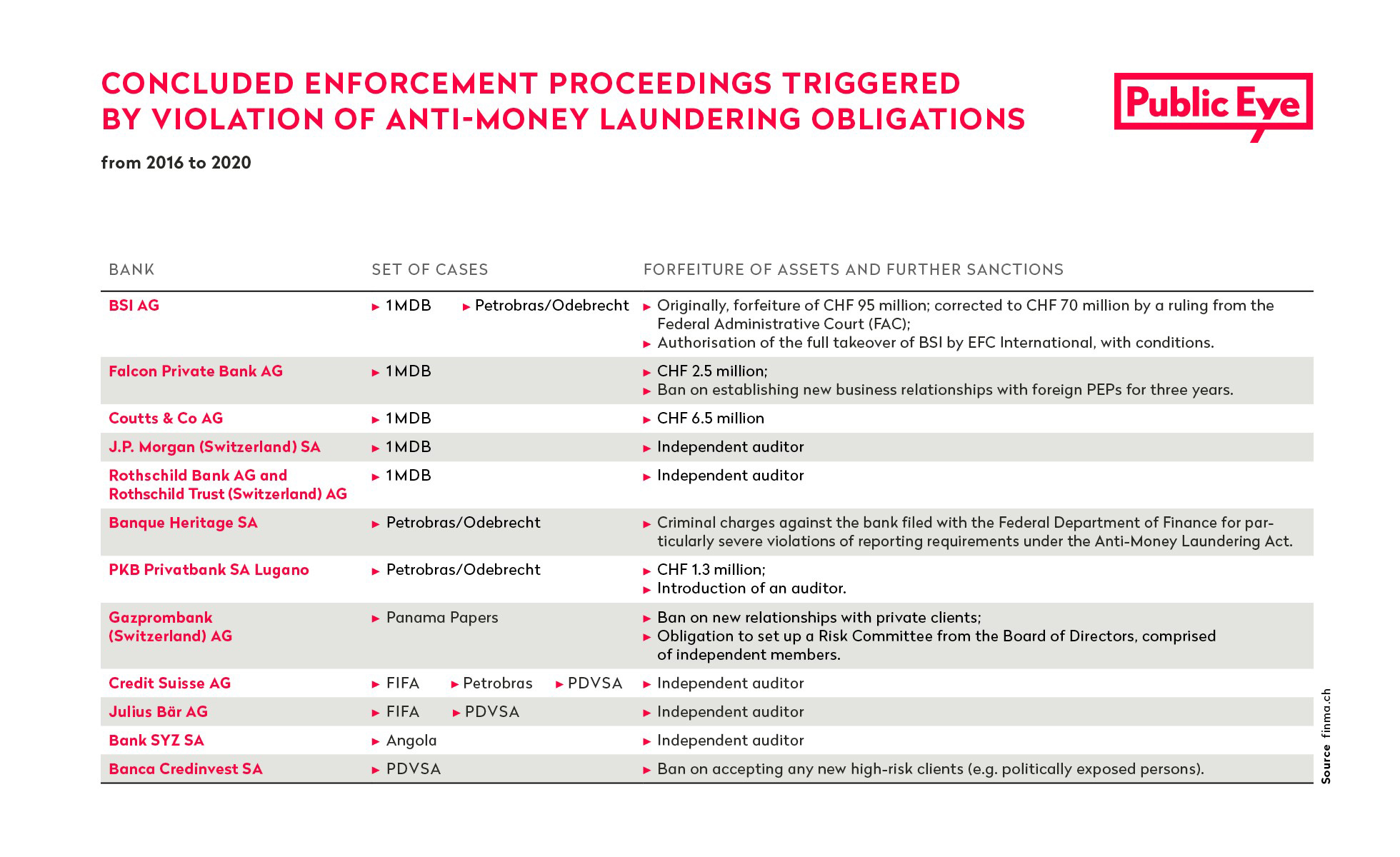

FINMA opened seven enforcement proceedings due to suspicion of violation of anti-money laundering obligations in the case of 1MDB alone. As part of these, severe irregularities were established in at least six banks and in some cases assets were forfeited. In relation to PDVSA, FINMA was in contact with 30 Swiss banks and initiated five proceedings.

It is noticeable that in recent years FINMA has scrutinised the anti-money laundering practices of banks under its remit more closely and has observed shortcomings more consistently. At the same time, the list shows that FINMA has barely forfeited any unlawfully obtained assets. FINMA generally imposes ‘sanctions’ that require financial institutions to improve internal processes under the supervision of an external auditor.

A bank rarely faces sanctions that carry significant implications and it seems these are reserved for small banks.

Is FINMA’s choice of sanctions influenced by the economic and financial clout of the financial institution in question? In no case has it disclosed the order in question; it has simply issued a press release announcing that proceedings have been concluded and publishing the main findings and measures. More transparency around this is essential.

©

Mark Henley

©

Mark Henley

Criminal proceedings and rulings against banks?

In Switzerland, criminal law also applies to banks. This fact should be a matter of course, but it is not reflected in criminal convictions. In recent years, there have been individual cases that were followed by convictions of banks’ individual compliance managers for violations of the Anti-Money Laundering Act. These convictions took place in cases where individuals had been reprimanded by FINMA for severe breaches of duty in relation to the fight against money laundering. However, the criminal proceedings never addressed the issue of inadequate organisation to prevent money laundering at affected banks. This is highly surprising given that – as outlined above – corporate criminal liability specifically applies to cases of inadequate organisation. Moreover, as the list above indicates, FINMA has identified such issues in numerous cases.

In recent years, FINMA has identified at times severe inadequacies in terms of internal organisation to prevent money laundering, yet to date only a single indictment – against the Falcon Bank – has been filed with the Federal Criminal Court. The trial was due to start in March 2021, but has been postponed until end of September 2021. There is another case relating to Credit Suisse AG. The Office of the Attorney General of Switzerland is accusing the bank of “failing to take all the reasonable organisational measures required to prevent the laundering of assets belonging to a criminal organisation and under the bank’s management” in relation to the business relationship between Credit Suisse and the Bulgarian ‘Cocaine King’ Banev.

The federal law enforcement authorities are investigating at least three financial institutions in connection with the Petrobras complex: PKB Privatbank, J.Safra Sarasin and Banque Cramer & Cie SA. They are all suspected of failing to implement all the reasonable organisational measures required to prevent money laundering.

To date there has been no indication of a clear will to use criminal law to implement the anti-money laundering legislation. Moreover, any system that continues to limit the fight against money laundering and dictators’ assets largely to voluntary self-regulation by banks is fundamentally questionable.

Credit scandal in Mozambique – and once again it involves Credit Suisse….

In the case of the Mozambican hidden debt scandal – which has Credit Suisse up to its ears in legal proceedings – the criminal and supervisory authorities once again failed to act themselves. It appears that the Office of the Attorney General (OAG) only assessed the case seriously after Public Eye filed a criminal complaint against Credit Suisse in April 2019. For only a month beforehand, the OAG had made the following statement, published in a Swiss newspaper, about Credit Suisse: “The OAG is not currently undertaking any national criminal proceedings”. This was justified by an assertion that the request for mutual legal assistance from Mozambique did not present sufficient grounds for suspicion.

It has since come to light that in February 2020 the OAG had opened criminal proceedings against unknown persons for money laundering in connection with the hidden debt scandal. In doing so, it had drawn on our criminal denunciation, suspicious activity reports filed with the Money Laundering Reporting Office Switzerland (MROS) and the request for mutual legal assistance sent from Mozambique, which had reportedly been insufficient a year earlier. It is not yet clear whether Credit Suisse will be held criminally liable in this case.